BuildingFintechFromZero

0 → 500K+

Users

Impact

Context

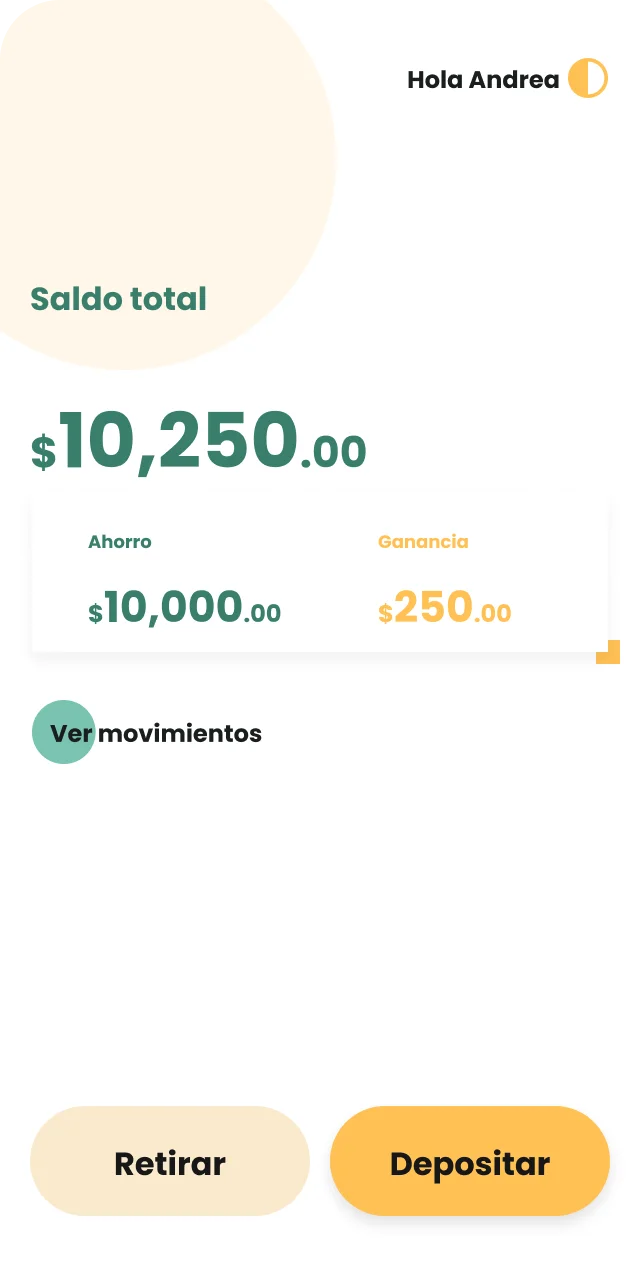

DINN — Actinver's digital investment app for first-time investors in Mexico

November 2018 – October 2020, founding phase

Product & Visual Designer on the founding team for DINN 2.0.

I owned the full brand identity — logo, visual system, color, type, tone of voice, motion — and designed the first version and every iteration of the product.

Strategy and product definition were collaborative: every design decision passed through business, legal, and growth before shipping.

The Problem

DINN 1.0 was functional and almost a year live, with near-zero users. No one had asked young Mexicans why they weren't investing — or how they wanted to.

The Research

Every competitor in Mexico was communicating in functional territory — rates, features, security badges. Nobody had claimed the emotional and educational space. Nobody was talking to young people about their relationship with money.

What the research told us about the target:

The Core Design Decisions

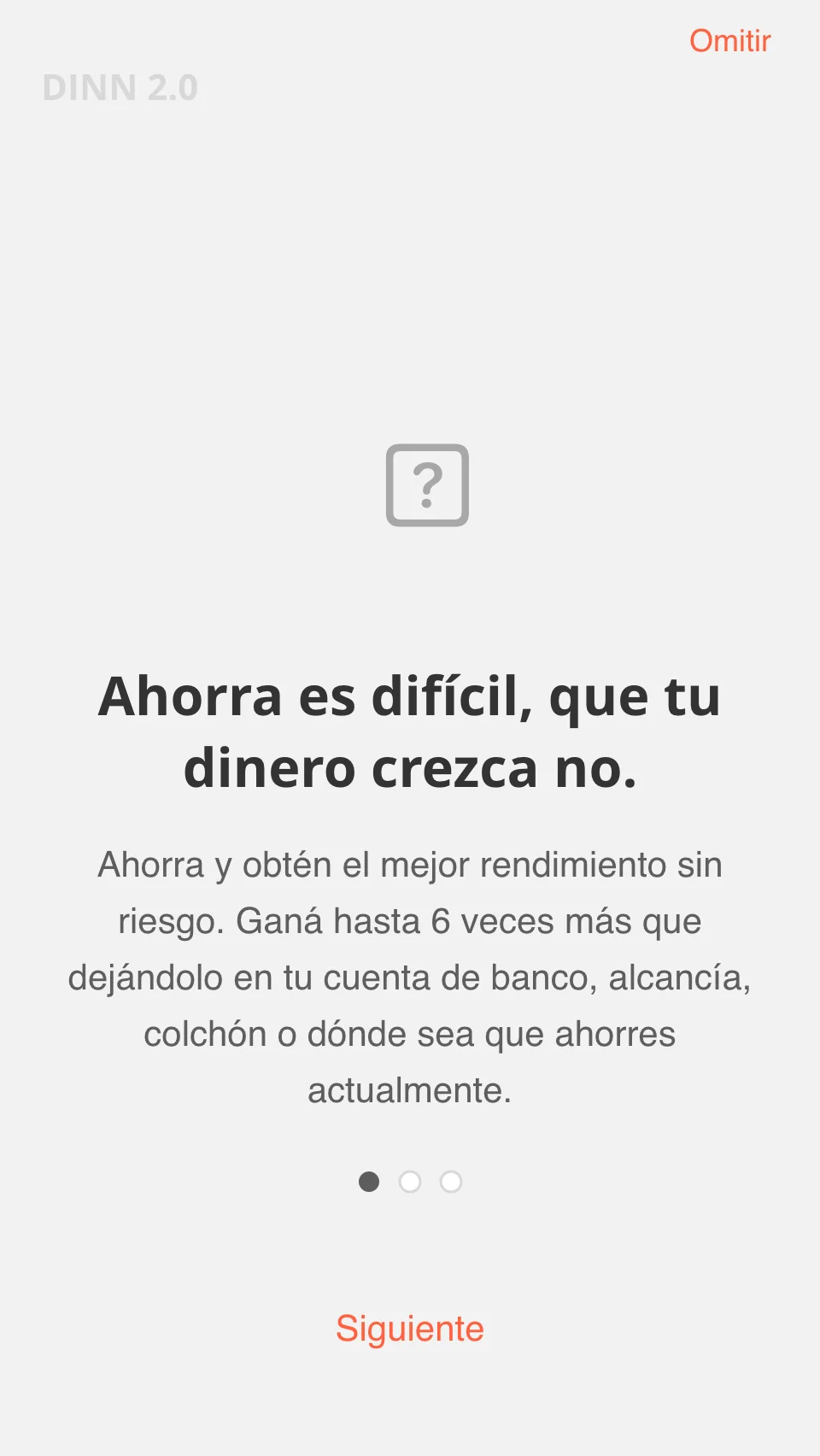

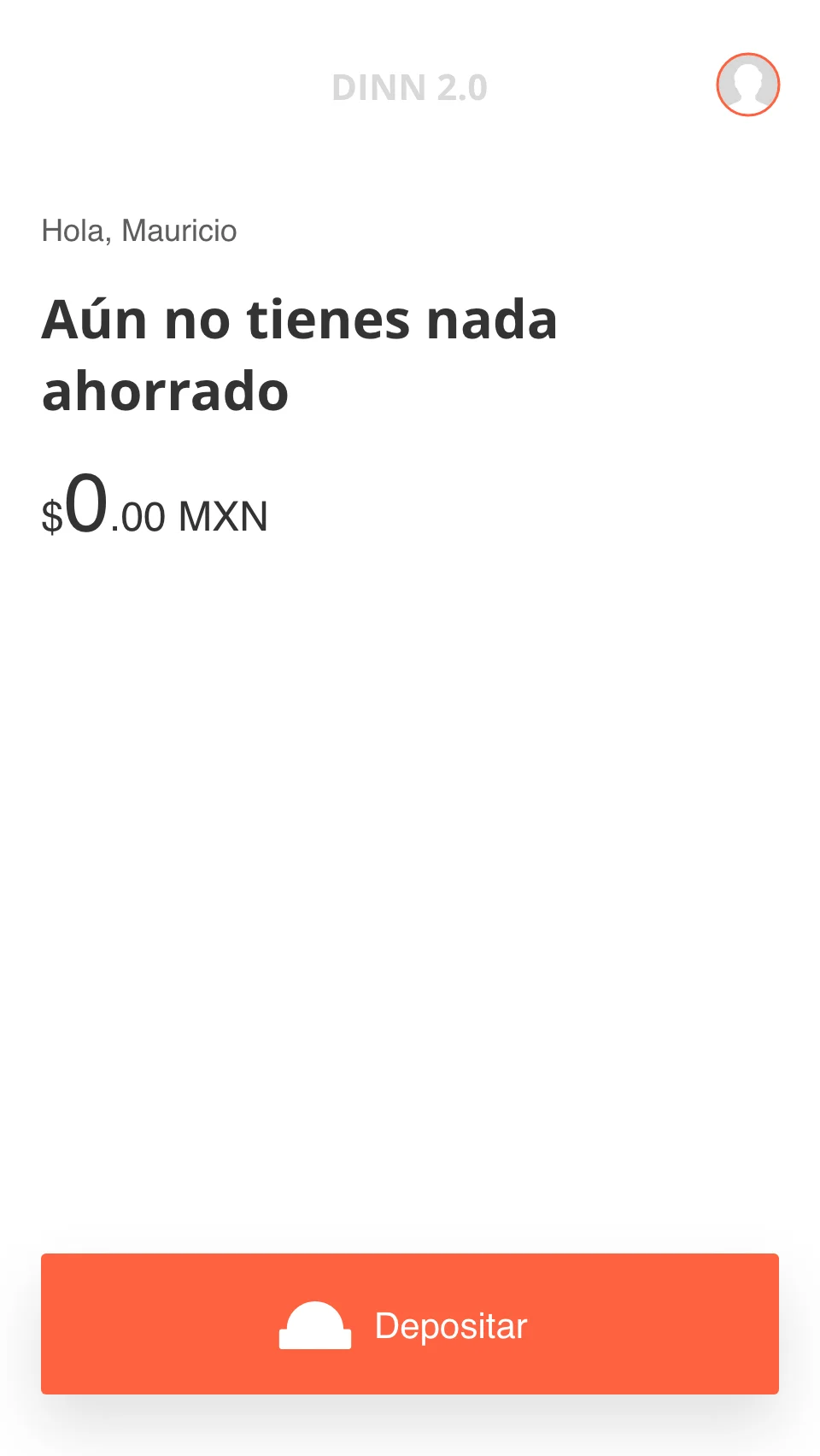

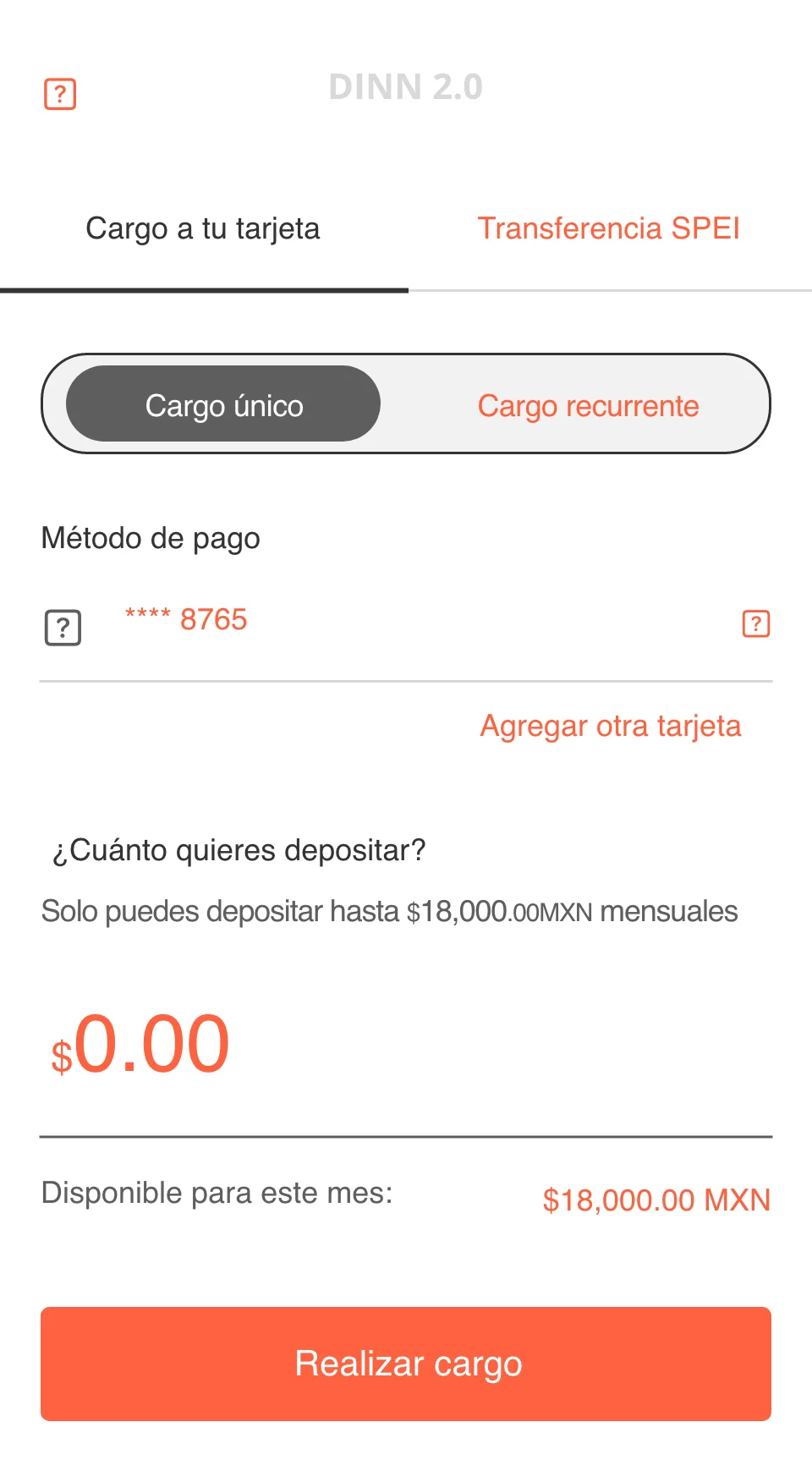

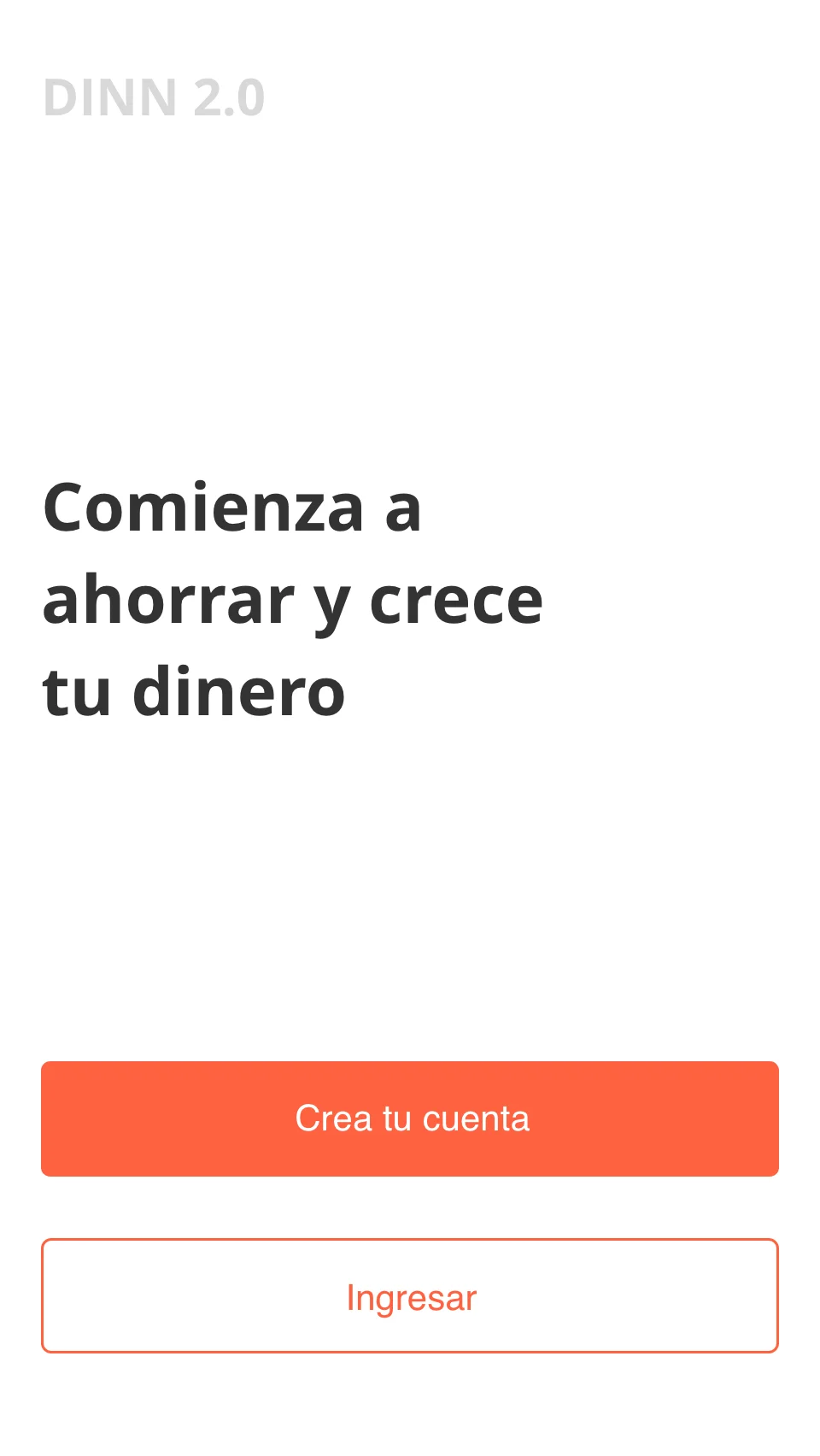

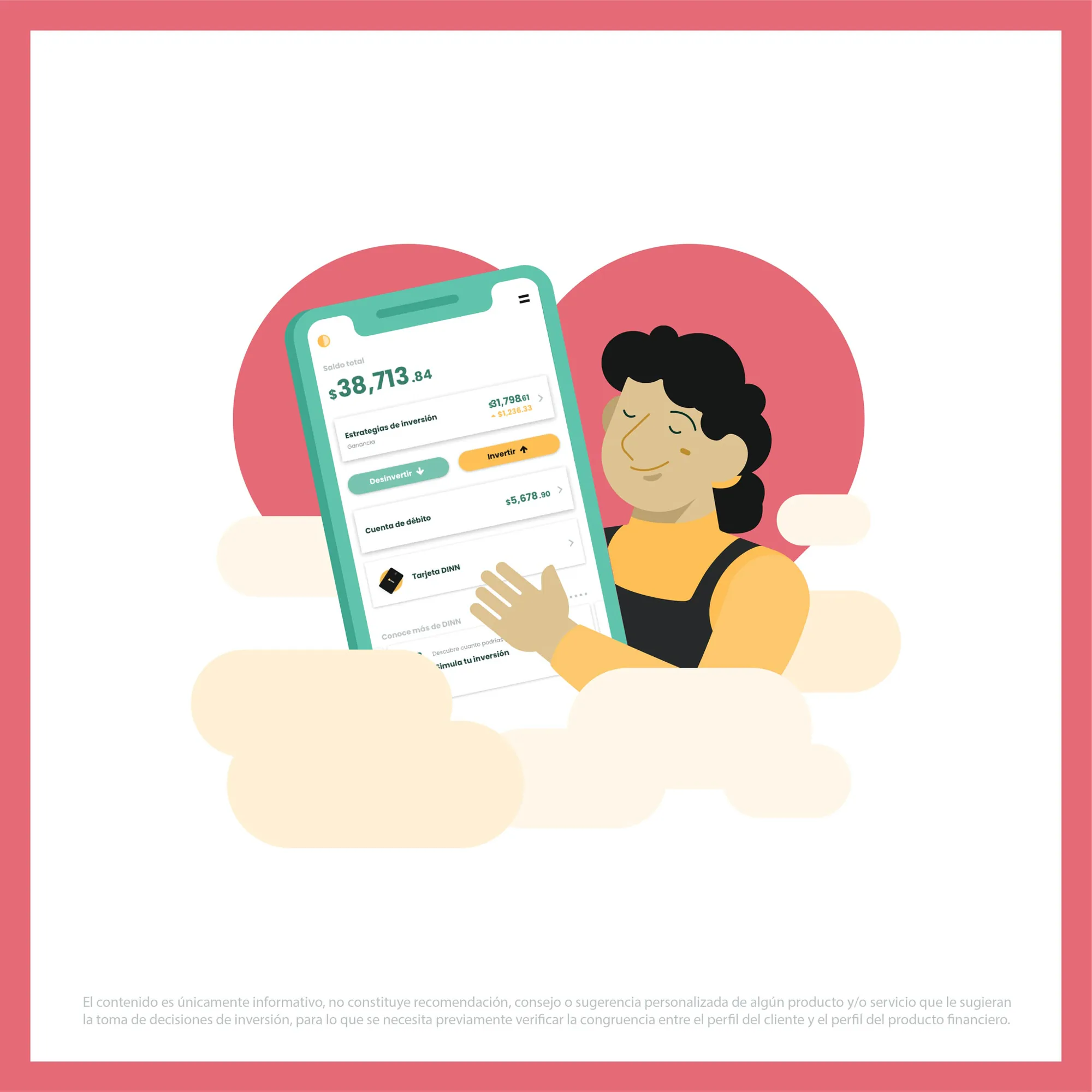

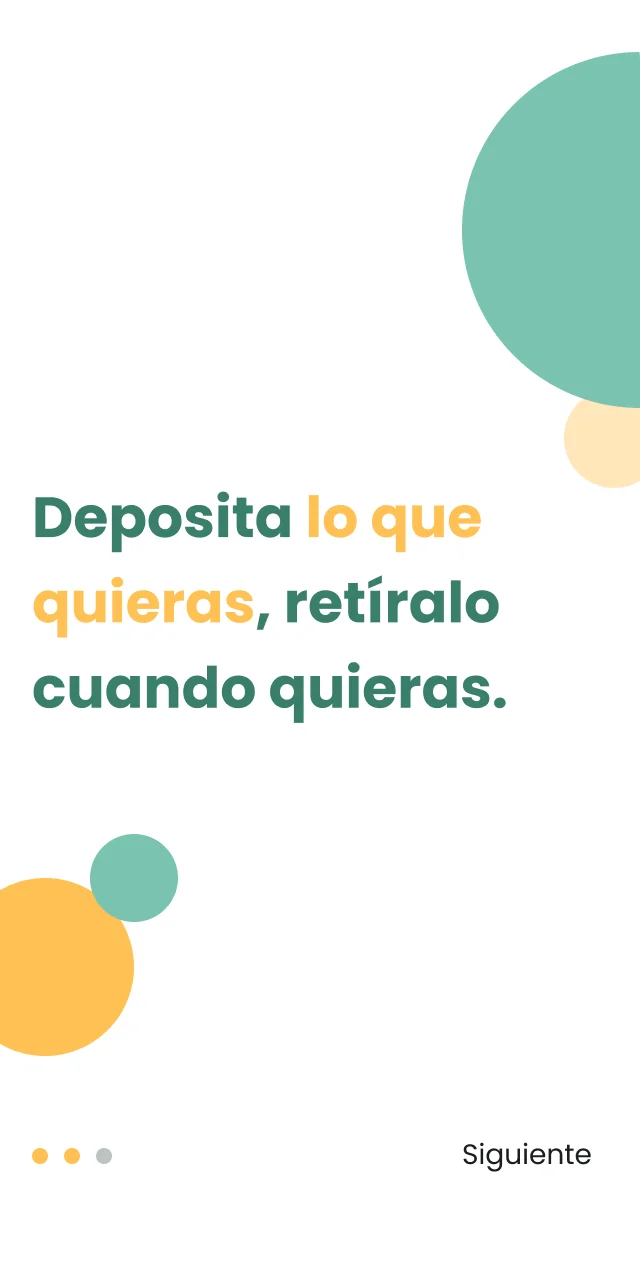

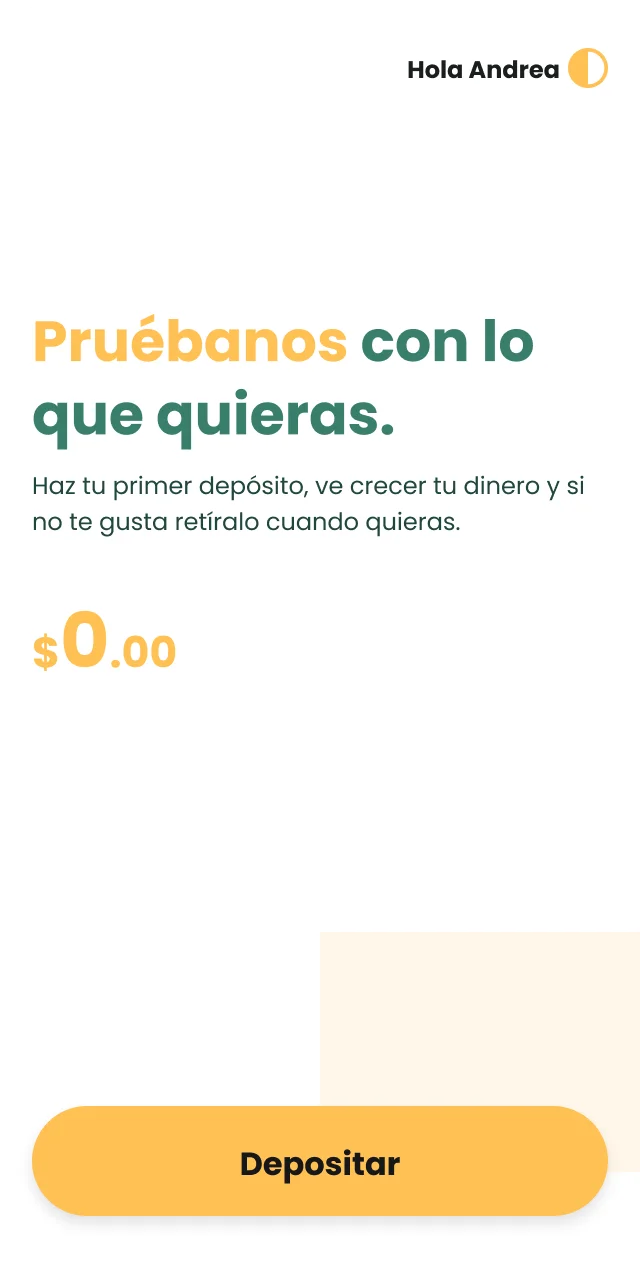

1. Don't build for investors. Build for savers who don't know they can invest. The target already had the behavior (saving) but not the mental model (investing). Product thesis: simple savings account + you earn returns. One step, no minimum.

2. Own the emotional territory. Every competitor talked rates and features. We positioned at the intersection of simple and earning: "DINN: Simple + Your money earns."

3. Design the behavioral change, not just the product. We used BJ Fogg's Behavior Model — Motivation, Ability, Trigger — as the launch framework, and mapped all three.

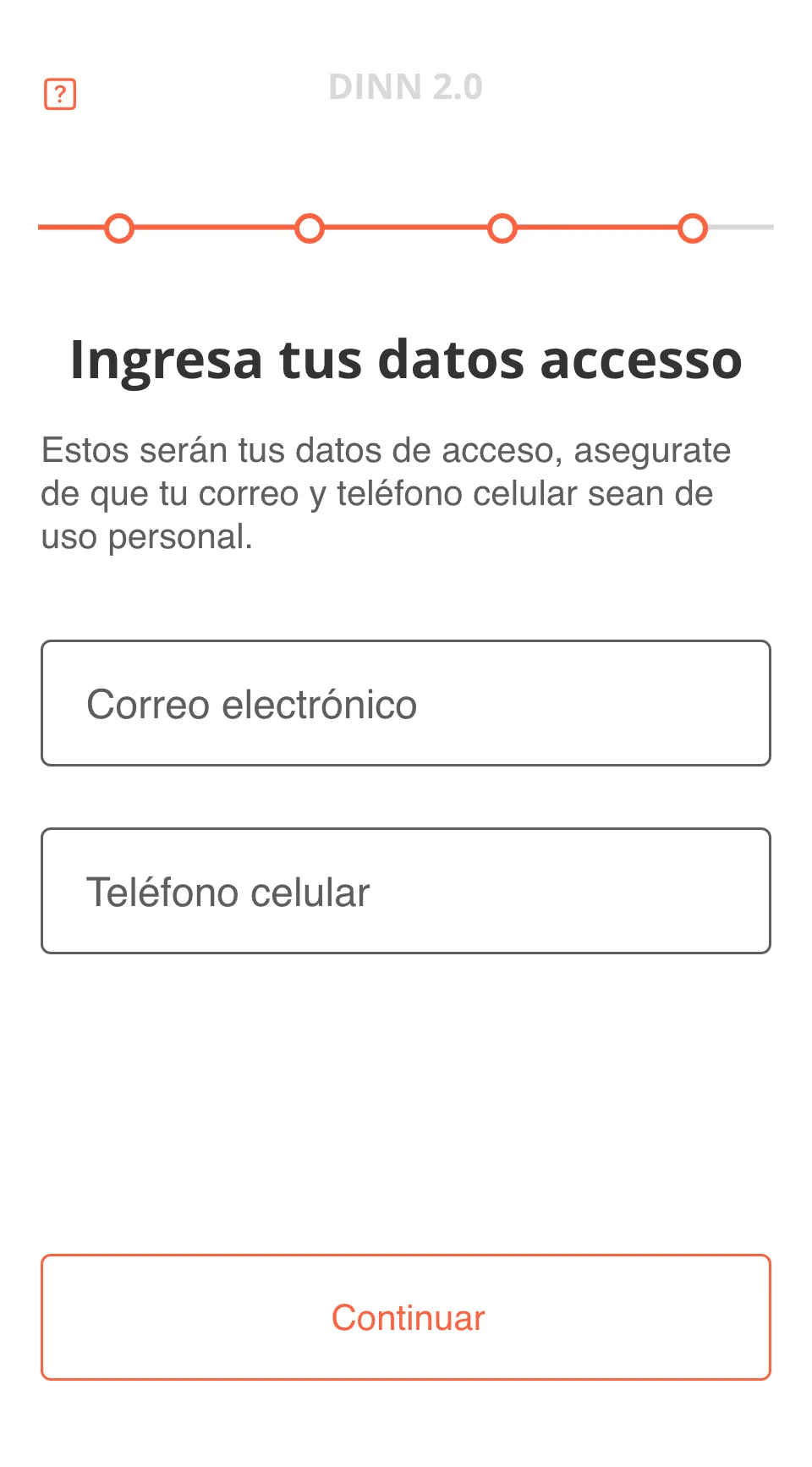

DINN 2.0 — Wireframes

Process

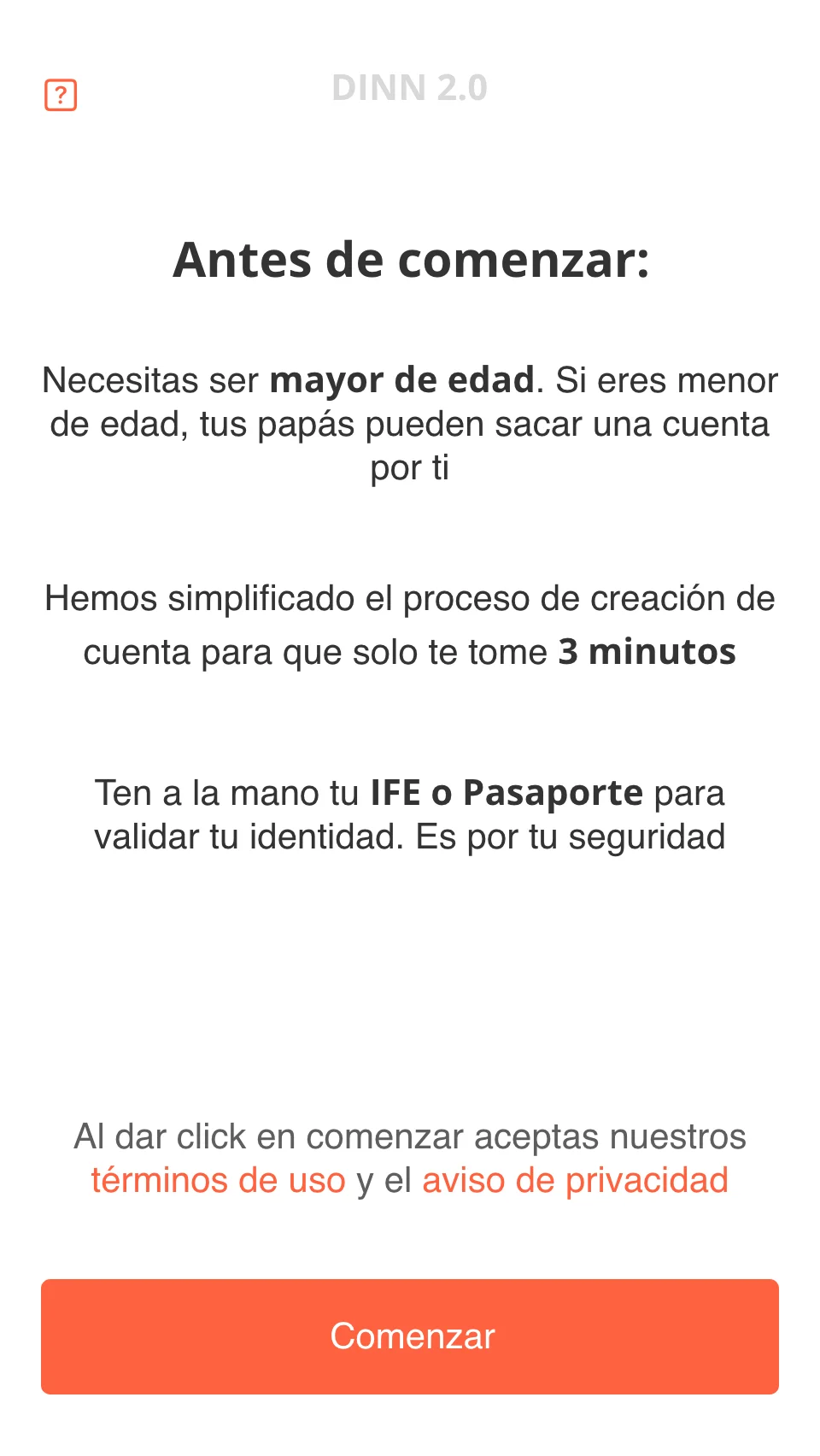

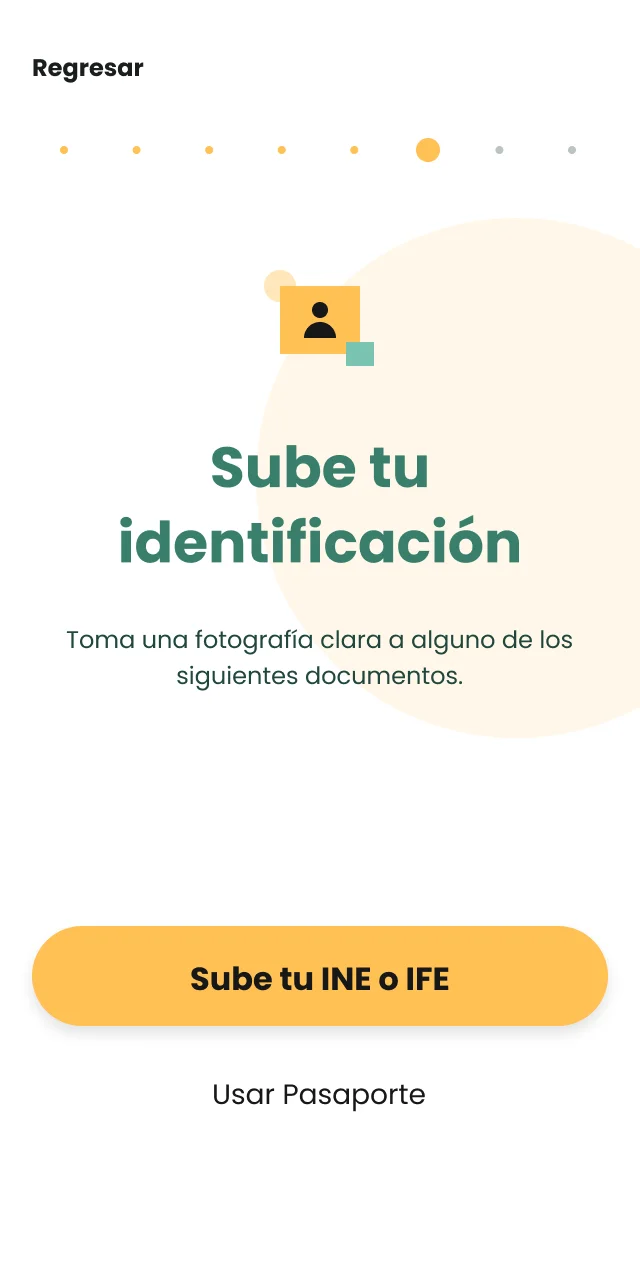

Brand and product were designed in parallel — the identity had to read simple and credible at once, a hard balance in fintech. Every element went through user testing before development.

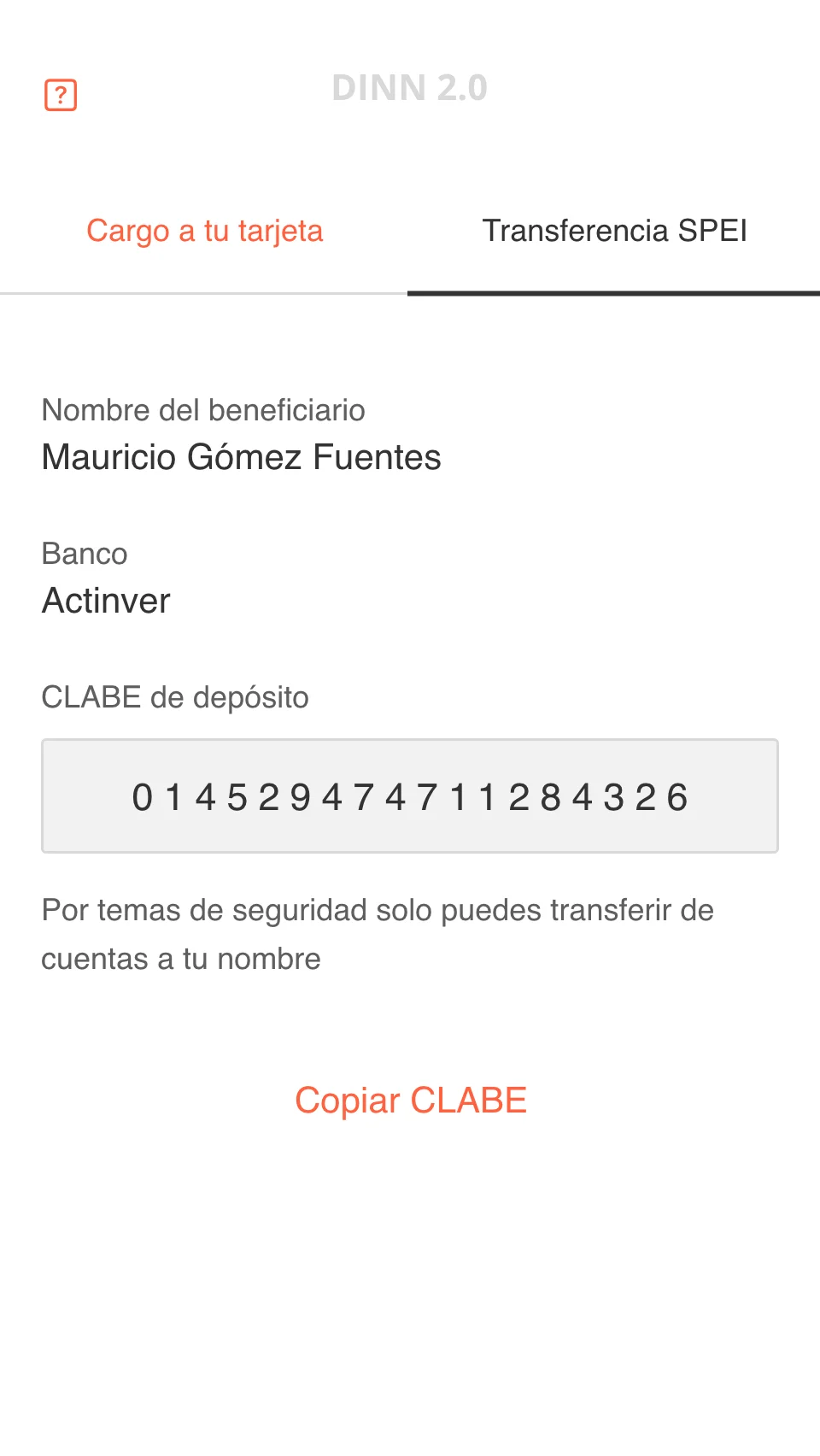

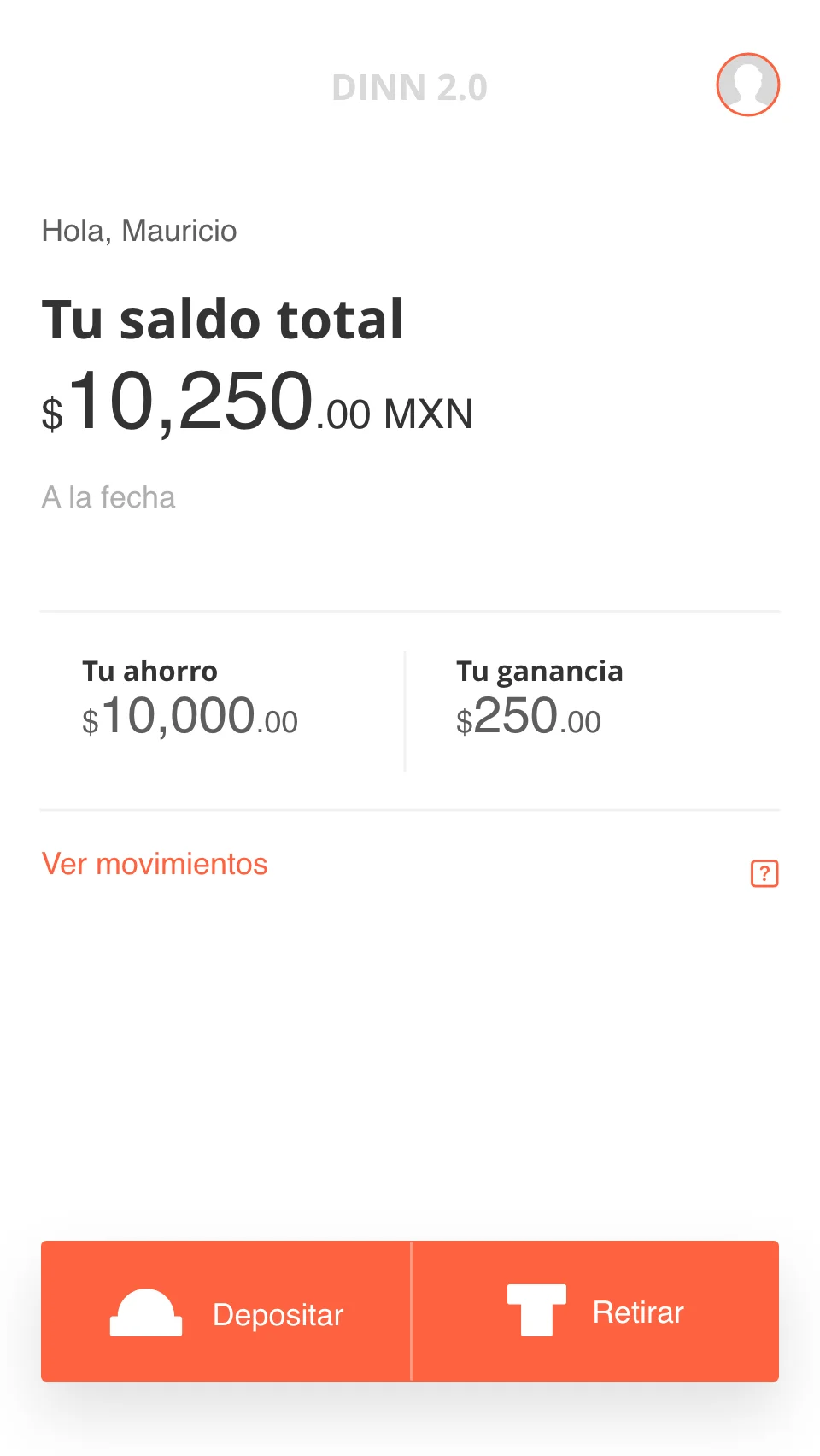

The product became the simplest in the market: sign up, deposit, and your money is automatically invested.

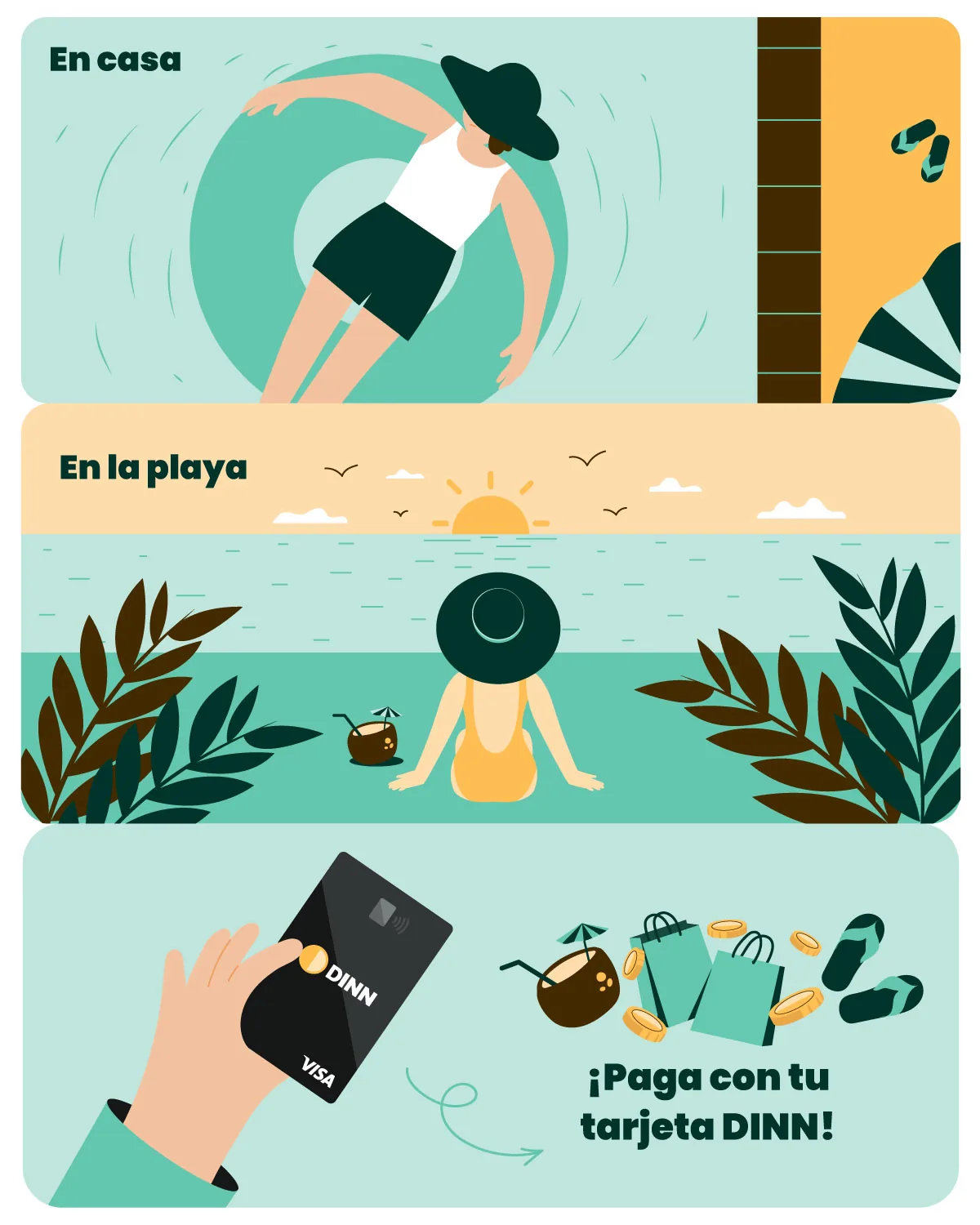

In early 2020 we launched the DINN debit card, so users could spend their money day to day.

Key Deliverables

Outcome

From a near-zero v1 to 500K+ users. The same insight drove all of it: meet people where their behavior already is, and remove the barrier — not the product — that stops the next step.

Reflection

DINN 1.0 didn't fail on the build. It failed on untested assumptions. The product was never just features — it was removing the barriers that stop a behavior from happening. Fogg's Motivation + Ability + Trigger is the most useful design model I've used in fintech.